What is a structured product or AMC and why does it matter?

Simply described, structured products are a contract with a bank or issuer and the contract has a pre-defined outcome that if certain conditions are met, an investor will receive a particular rate of return or coupon. As such they have become an integral part of many institutional and professional (non-retail) investor portfolios.

An actively managed certificate (AMC) is a debt instrument issued by a special purpose vehicle as a structured product comprising a portfolio of underlying assets (liquid securities, bonds, funds, shares, derivatives, currencies, etc.). Usually the AMC follows a defined composition of underlying assets or an index which changes over the time at the discretion of an external asset/portfolio manager.

Interestingly, this form of structured product can potentially address investors’ needs in a similar manner to a fund and also have easy integration of several structured products which can be actively managed simultaneously and be mixed with further assets or instruments like equities, bonds or funds but without the same legal or regulatory overlay as a conventional collective investment fund.

Modern AMCs also have limited SPV issuer risk without being subject to limitations imposed by traditional issuers or funds. Structured products can also provide exposure to non-bankable assets ranging from forestry, machinery, or hotel financing, to peer-to-peer loans and crypto are now investible on a balance sheet-neutral basis.

As the alternative funds space has become more and more regulated, particularly in relation to the marketing of funds in EU jurisdictions even to non-retail investors, managers are seeking cost-effective structuring that meets the needs of institutional and professional investors in a proportionate way where less investor protections are justified.

If the investor base of a manager is able to invest in structured debt products rather than in a fund interest, products such as AMCs may well offer a fascinating alternative to a conventional fund.

Typical features

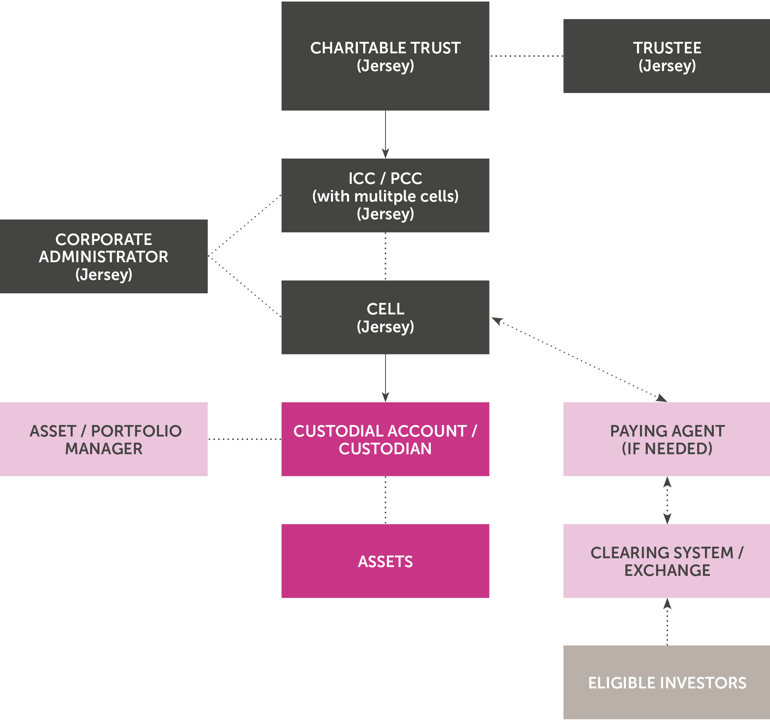

- Private corporate cell company issuer where ownership of the cell company and cell are both orphaned – i.e. owned by a charitable trust and off balance sheet

- Issuer issues debt rather than equity

- Usually there are at least two Jersey-resident directors and board meetings take place in Jersey (ensuring compliance with Jersey's economic substance regime)

- Administered by a corporate services provider in Jersey

- Cleared through a clearing system and/or listed on an exchange such as The International Stock Exchange (TISE) in the Channel Islands

- Offered to 'professional investors' or with minimum consideration/denomination of EUR100,000 (or currency equivalent) among other criteria that can ensure light touch offering memorandum content requirements

- The asset or portfolio manager need not be regulated in Jersey (although it will have relevant expertise and may be regulated in its home jurisdiction)

- Audit not required (although usually policy dictates that the terms enable at least 10% by value of the holders to require one at the requesting holders' expense)

- No set custody requirements

- Not treated as a collective investment fund under Jersey law provided the requirements of an exemption are met and service providers can be exempt as regards carrying out investment business

Example structure

Advantages

- Can access a wide range of institutional capital due to the use of the clearing system/ and/or listing but without qualifying as a fund therefore resulting in lighter-touch regulation and more limited legal, regulatory and administration costs – less drag on return

- Low AUM less of a factor in relation to obtaining service provision and cost profile

- An ability to trade the relevant securities and provide a degree of liquidity (depending on the exchange or clearing system)

- Fast time to market relative to fund launches – possible same-day incorporation and then can be as quick as within 5-10 business days from submission of the regulatory application

- Enables institutional investors to gain indirect exposure to an asset class which they couldn’t hold directly but with active management of the asset

- Bankruptcy remote 'off balance sheet' structure can limit the risks of direct exposure to underlying assets, particularly in volatile asset classes such as crypto

- Proportionate regulation of the issuer relative to the experience and profile of investors when compared to a similar fund structure

- Can have a potentially unlimited amount of investors

- The offering memorandum won’t necessarily require prescribed detailed content requirements (unless required by the relevant exchange or clearing house) or have to deal with AIFMD requirements (including disclosure and reporting)

- Can introduce varying degrees of investor protection through elements such as the contractual terms, security trustee arrangements, paying agents, custodians etc

- Notes can be structured to provide different types and timing of return and redemption rights depending on the nature of the underlying assets

- Can help build track record of unregulated investment managers and advisers

- Can be put into a platform in a more straightforward way than conventional funds and utilise standard Jersey companies, ICC and PCC models depending on preference

- Different asset managers can be used across different cells in the same cellular structure and can be designed to facilitate highly customized risk-return objectives

- More limited and cost-effective compliance requirements for the issuer due to the fact that investors are accessing the issuer through a clearing house or exchange rather than directly.

Other considerations

- A typical Jersey issuer will be subject to Jersey income tax at a rate of 0 per cent. Holders should generally not be subject to any tax in Jersey in respect of the holding, sale, redemption or other disposition of such securities

- No stamp duty is levied in Jersey on the issue, transfer, acquisition, ownership, redemption, sale or other disposal of the securities

- Jersey is an OECD territory but although it has a special relationship with the UK, is not part of the UK and is outside the EU. EU directives do not apply directly

- There is a long standing and consistent regulatory policy towards securities issuance and the Jersey Financial Services Commission has a lot of experience with structured products, CLO and related securitisation structures

- Jersey respects the integrity of bankruptcy remote vehicles and is well known to the rating agencies and for ISDA transactions

- A variety of flexible legal forms are available in Jersey including charitable trusts, corporates, cell companies, unit trusts, LLCs and limited partnerships, facilitating accessibility to various markets and investor preferences

- Company law in Jersey has English statutory origins (therefore familiar to advisers and clients) although it has evolved to be more flexible in areas such as distributions and changes to capital amongst others

- Far lighter touch than the regulatory approach to similar vehicles in EU jurisdictions, keeping costs down

- Deep local expertise across multiple crucial disciplines of legal, administration, tax, accountancy and regulatory service provision which provides an end-to-end solution at a competitive price point

- Quality and responsiveness of service provision that has a 'can do' service ethos, driven by its natural and long-standing affinity with the City of London

- Regulatory certainty through appropriate governance and substance and the Jersey Financial Services Commission (JFSC) is an approachable, globally respected and co-operative regulator, supervising pragmatic regulation that meets international standards (IMF, IOSCO, ESMA, FATF)

- Legal certainty through a respected and long-established legal and court system that ensures that any enforcement or disputes can be managed and dealt with appropriately

About this guide

This guide gives a general overview of this topic. It is not legal advice and you may not rely on it. If you would like legal advice on this topic, please get in touch with one of the authors or your usual Collas Crill contacts.

About Collas Crill

We are a leading offshore law firm. We are easy to do business with and give practical advice to overcome tough challenges. Through our network of offices, we practise British Virgin Islands, Cayman Islands, Guernsey and Jersey law.