For several years, private trust companies have been the vehicle of choice for administering the assets of wealthy families. Many variants have emerged, as each host jurisdiction has its own requirements for exempting a private trust company from its licensing and regulatory regime for trust companies offering trust services to the public. One of the main attractions of private trust companies is that decisions relating to the underlying trusts are made by directors, who are carefully chosen by the patriarch or family, often mirroring the boards of the operating companies within the structure.

The Control Issue

Where the private trust company is incorporated as a company limited by shares, the shareholder or shareholders will typically have the right to appoint and remove the directors. Too much control can have tax implications, so many clients will need to be able to demonstrate that they do not control the trustee of the trusts established for the benefit of their families. This may rule out family members from being shareholders of their private trust company. Where being seen to be in control is not an issue, for example where the family is resident in a low-tax jurisdiction, direct ownership by the family of the shares of the private trust company may be possible, but can lead to succession issues on the death of a shareholder.

The founder

The founder could be the patriarch, but does not need to be, as any person, including a corporate entity, can be the founder. The founder endows the initial capital (a Guernsey foundation does require some initial capital, in the same way as a trust), but this does not automatically give them any ongoing interest in the foundation. Any continuing role for the founder, where appropriate, must be set out in the foundation’s constitution, which consists of a charter and rules similar to the memorandum and articles of association of a company.

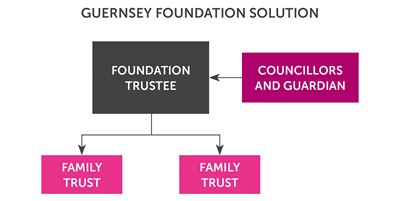

Council

The foundation is run by its council in the same way that a company is run by its board of directors. The council must comprise at least one councillor, and councillors can be individuals or corporate bodies; the details of the councillors are made public on the Foundations Register. The councillors owe a duty to the foundation to act in good faith in the exercise of their functions.

Guardian

As the foundation trustee will not have any beneficiaries, a guardian will have to be appointed. The role of the guardian is similar to the role of the enforcer of a purpose trust: under the law the guardian has a duty to the founder to act in good faith and en bon père de famille to enforce the constitution and the purpose, and in the exercise of their functions.

The guardian can be given the power to appoint and remove directors; the enforcer of a purpose trust cannot enjoy such a power directly as they will not be a shareholder (although they could threaten to exercise a power to remove the trustees of the purpose trust to ensure that their wishes are enforced). The guardian cannot, for obvious reasons, be a councillor.

The resident agent

If neither the guardian nor any of the councillors are Guernsey- licensed fiduciaries and none hold a sufficiently senior position in a Guernsey licensed fiduciary business, the foundation must appoint a Guernsey-licensed fiduciary as its resident agent. This is similar to a private trust company where a licensed fiduciary will provide the registered office and satisfy any requirements for local involvement, as well as providing trust and corporate administration services to the structure. It is not a requirement under the law to have a Guernsey licensed fiduciary on the council, though it may be sensible, as the foundation will be exercising fiduciary powers in its role as trustee.

Final thoughts

The foundation trustee will thus be run and managed in a similar way to a private trust company with the involvement of a local licensed fiduciary, but with the significant advantage that, as an orphan vehicle, it does not have any owners or controllers. Where it is important to demonstrate separation between the family and the foundation acting as trustee of trusts for its benefit, family members should not hold any positions or reserve any powers under the foundation.

As the Guernsey foundation offers a simple and practical solution to the control issue, it is an attractive variant of the classic private trust company structure.

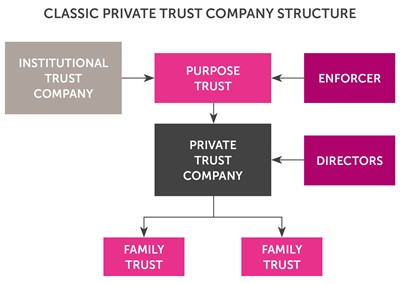

The most common solution to the control issue, until now, has been to hold the shares through a purpose trust. This creates extra layers of administration and cost, as it involves an institutional trust company acting as the trustee of the purpose trust. In some jurisdictions there is also doubt as to whether holding an asset is a valid purpose; in such circumstances another purpose may need to be added. To address this, several jurisdictions, including Guernsey and Jersey, have amended their purpose trust laws to expressly provide that a valid purpose includes the holding or ownership of property and the exercise of functions. The Bahamas have gone further and created the Bahamas Executive Entity (BEE) as an entity seemingly designed solely to hold the shares of a private trust company.

An alternative has been to incorporate the private trust company in the form of a company limited by guarantee. The problem with this is that, as the company has no shareholders, the directors, for the time being, are the only people who can appoint successor directors and remove their fellow directors, so outside control is not possible. Another variant has been for the private trust company to have separate classes of shares, with one class having the right only to appoint and remove directors, but no other rights - and particularly no economic rights.

Explaining purpose trusts, BEEs or companies limited by guarantee to entrepreneurial clients can often mean that a succession-planning meeting involving a private trust company falls at the final hurdle for reasons of complexity. Guernsey has the solution.

The Guernsey Foundation solution

A new and much simpler variant is now available in Guernsey that removes the need for any layers above the private trust company – no purpose trusts, no BEEs, no anything. Just establish a foundation under the Foundations (Guernsey) Law 2012 (the law) with the sole purpose of acting as trustee of trusts for the benefit of an individual family. This is the foundation trustee. The law makes it clear that a Guernsey foundation, upon establishment, has its own legal personality, independent from that of its founder and any foundation officials.